SFY 2026-27 General Appropriations Act

Overview

On Friday, May 29, the Florida House and Senate agreed to a budget for State Fiscal Year (SFY) 2026-27. The budget is the culmination of many rounds of budget negotiations throughout the legislative session. The Florida Legislature is constitutionally required to pass a state budget, officially titled the General Appropriations Act during the annual regular session. This year, due to major allocation disagreements, the Legislature adjourned Sine Die during the regular session and reconvened Special Session E on the state budget. Legislative leaders met over several weeks to hammer out budget details including finalizing the budget, implementing, and conforming bills over the Memorial Day holiday.

The SFY 2026-27 General Appropriations Act, HB 5001E, totals $114.5 billion and represents a 0.6% decrease from the previous SFY 2025-26 General Appropriations Act. However, the budget is subject to potential line-item vetoes by the Governor.

To view all Budget Conference Reports for Special Session E, House Budget and Senate Appropriations

Contained within the budget are changes to the Florida Retirement System (FRS) including a mandate on counties to comply with increases in Cost-of-Living Adjustments (COLA) for Special Risk Class. Net impacts from the FRS bill are $102.5 million for counties statewide.

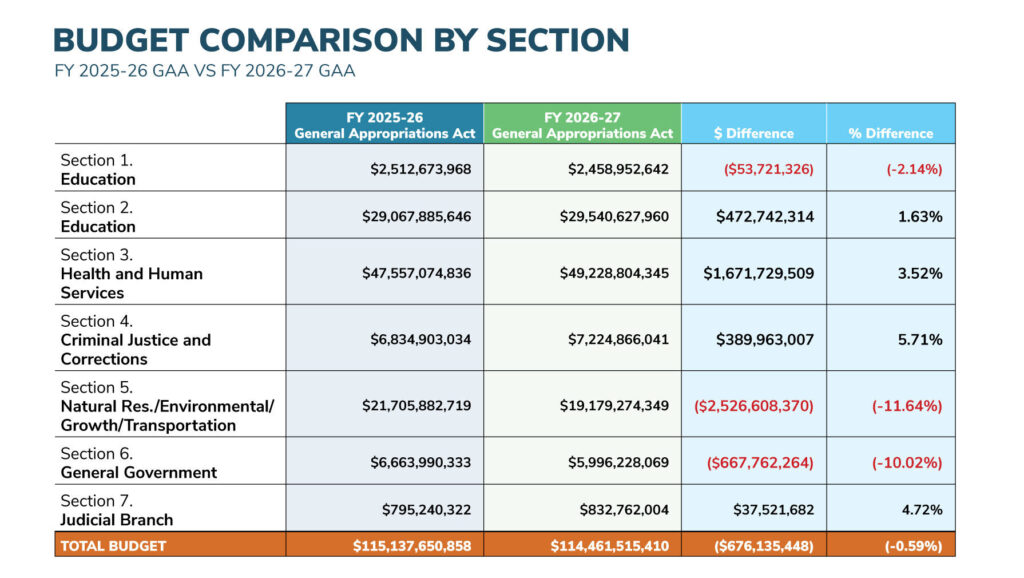

The chart below summarizes a comparison of this year’s SFY 2026-27 budget and the budget approved for SFY 2025-26.

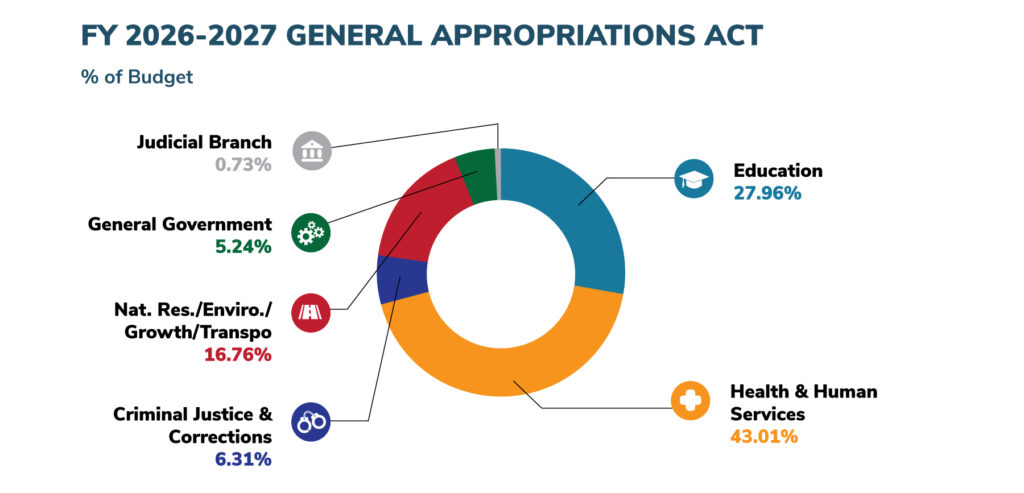

Health and Human Services received the largest portion of funding for the budget in SFY 2026-27, totaling approximately $49.2 billion. This represents a 3.5% increase in appropriation from the current year. All educational programs and services combined received the second-largest amount of funding, totaling approximately $32 billion. This represents an increase of approximately 1.3% from the current fiscal year.

Finally, Natural Resources, Environmental Issues, Growth Management and Transportation expenditures represent the third-largest portion of the budget in SFY 2026-27, with funding equaling approximately $19.2 billion, a decrease of approximately 11.6%. The budget reflects a reduction from the prior-year baseline, primarily within transportation and environmental capital outlay categories.

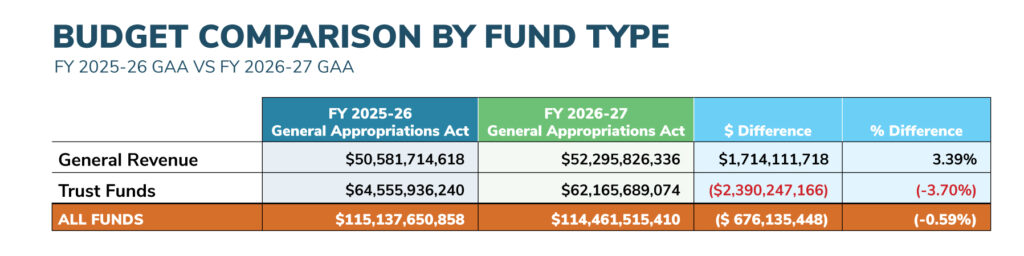

General Revenue expenditures for the SFY 2026-27 budget equal approximately $52.3 billion, while trust fund expenditures total approximately $62.2 billion. Compared to the SFY 2025-26 budget, General Revenue spending increased by approximately 3.4%, while trust fund spending decreased by approximately 3.7%. The chart below compares expenditures between the SFY 2026-27 budget and the previous year’s budget for SFY 2025-26 by fund type.

County Funding Highlights

Health, Safety, & Justice

Shared County/State Juvenile Detention: The conference budget estimates the county-funded portion of detention center costs at approximately $85.9 million through the Shared County/State Juvenile Detention Trust Fund. This represents an estimated increase of approximately $7.7 million, compared to the SFY 2025-26 budget estimate of $78.2 million. Additionally, the budget provides approximately $3.8 million in General Revenue for grants to fiscally constrained counties for detention center costs.

Community Substance Abuse and Mental Health Services: Funded at approximately $1.387 billion in total funds. This is generally consistent with the prior-year baseline of approximately $1.4 billion. Proviso requires additional reporting on opioid settlement trust fund expenditures and specialty treatment teams, including county or circuit served, target population, individuals served, encounters, contract amount, and funding type.

Community Action Treatment Teams: The budget provides $41.6 million in General Revenue for CAT teams, which provide community-based services for children and young adults with mental health and/or substance abuse diagnoses. Funding is essentially unchanged from the prior fiscal year.

Public Safety, Mental Health, and Substance Abuse Local Matching Grant Program: The budget provides $15 million in General Revenue for the local matching grant program. This is the same amount as the SFY 2025-26 budget and remains a key county-relevant funding source for programs serving adults or youth in behavioral crisis or at risk of entering the criminal justice system.

Crime Lab Services: The budget funds Crime Lab Services at approximately $86.7 million total funds, an increase from the prior-year baseline of slightly more than $82 million. The appropriation includes aid-to-local-government funding for criminal investigations and related forensic investigative support.

Homeless Programs Challenge Grants: The budget provides approximately $20 million in General Revenue for Homeless Challenge Grants. This is flat compared to the SFY 2025-26 budget.

911 and E911 Grants: The budget distributes approximately $121.8 million for local wireless 911 systems, approximately $14 million for local non-wireless E911, and approximately $28 million for county prepaid wireless 911. The wireless 911 distribution is essentially flat compared to the prior-year baseline, while non-wireless E911 is approximately $1.6 million lower than the prior-year amount identified by FAC. The budget also provides approximately $2.8 million in General Revenue for public safety answering point upgrades in fiscally constrained counties.

Emergency Management Grants: The budget provides $500k to provide baseline capabilities allowing fiscally constrained counties access to WebEOC through the state hosted web application. The back of the bill carries forward any unexpended funds from the prior fiscal year on this issue. Additionally, the budget provides $2.1 million in General Revenue for the state’s alert and notification system.

AIDS Drug Assistance Program (ADAP): The budget includes funding and oversight language for the AIDS Drug Assistance Program within the Department of Health. The budget supports HIV/AIDS prevention and treatment services, while back-of-the-bill language provides $75 million in nonrecurring Grants and Donations Trust Fund dollars to maintain access to HIV/AIDS medications for eligible low-income individuals. Funds may be used for direct medication distribution, including through County Health Departments and contracted pharmacies for uninsured individuals, as well as medication co-payment and deductible assistance for insured individuals. The language maintains program eligibility at 400 percent of the Federal Poverty Level, caps enrollment in the direct medication provision at 21,000 individuals, and reappropriates any unexpended balance remaining on June 30, 2026, for the same purpose in SFY 2026-2027. The budget also includes enhanced oversight requirements, including monthly ADAP reporting by the Department of Health and an OPPAGA evaluation of program operations, fiscal sustainability, medication access, rebate strategies, formulary and eligibility options, clinical outcomes, and potential restructuring options. The OPPAGA evaluation is due January 31, 2027.

Agricultural & Environment

Water Projects / Wastewater, Stormwater, Septic-to-Sewer, and Drinking Water: The SFY 2026-2027 budget allocates approximately $380.4 million for named water projects, including $350 million from the Water Protection and Sustainability Trust Fund and $30.4 million from General Revenue.

Water Quality Enhancement and Accountability: The SFY 2026-2027 budget allocates $800,000 from the General Revenue Fund to expand statewide water quality analytics for nutrient over-enrichment assessment and the water quality information portal, including a statewide flood vulnerability and sea level rise data set. This is a reduction from the $10.8 million allocated in the SFY 2025-2026 budget.

Water Quality Improvement Projects: The SFY 2026-2027 budget allocates $20 million from General Revenue for septic to sewer and wastewater projects, that will improve the water quality of Biscayne Bay. The budget also allocates $25 million from general revenue for water quality projects in the Indian River Lagoon.

Small County Wastewater Treatment Grants: The SFY 2026-2027 budget provides $10.7 million total funds, including $2.72 million in General Revenue and $8.0 million in Federal Grants Trust Fund. General Revenue includes $800,000 for sand and grit removal grants and $1.92 million for mapping and loss estimation in publicly owned utilities. The sand and grit removal program is distributed first-come, first-served with local match, but match waiver is allowed for publicly owned utilities in rural counties and impoverished counties and municipalities.

Total Maximum Daily Loads: The budget provides $20 million in General Revenue and approximately $1.2 million from the Land Acquisition Trust fund for TMDL projects, with authority for DEP to include innovative water treatment projects and cost-share funding for innovative nutrient removal projects. This is down from the SFY 2025-26 budget providing $25 million.

Harmful Algal Blooms: The budget provides approximately $18 million across red tide management, innovative technologies, and county HAB emergency response grants. This includes $5 million specifically to assist county government responses to emergency conditions associated with harmful algal blooms, including red tide and blue-green algae. This is down from the SFY 2025-26 budget of $25.0 million.

Springs Restoration: The SFY 2026-27 budget allocates $50 million for land acquisition to protect springs and for capital projects that protect the quality and quantity of water that flows from springs. This is unchanged from the SFY 2025-26 budget.

Alternative Water Supply: The budget provides $50 million in General Revenue for the water supply and water resource development grant program. Funding is directed to help communities plan for and implement conservation, reuse, and other water supply and water resource development projects, with priority for regional projects in areas of greatest need and projects that provide the greatest benefit. This is unchanged from the prior-year budget.

Biosolids Grant Program: The SFY 2026-2027 budget allocates $5 million dollars for the Biosolids Grant program as authorized in section 403.0674, Florida Statutes.

Resilient Florida: The budget provides $160 million from the Resilient Florida Trust Fund for the Statewide Flooding and Sea Level Rise Resilience Plan, an increase of approximately $10 million compared to the prior-year budget. The budget also provides $10 million for Resilient Florida planning grants, a $10 million reduction from the prior-year budget.

Florida Forever / Land Conservation: The budget does not include a stand-alone Florida Forever appropriation in the main DEP budget. However, the bill provides significant conservation funding through the Land Acquisition Trust Fund, including $200 million for Conservation and Rural Land Protection Easements and Agreements, $2.5 million for the Working Waterfronts Program, and a back-of-the-bill reappropriation of unexpended land acquisition funds that provides $225 million for rural land protection easements and directs remaining funds toward specified conservation acquisitions, including projects on the Florida Forever Priority List.

Beach Projects: The SFY 2026-2027 budget allocates approximately $64 million dollars for beach and inlet management projects.

Mosquito Control: The SFY 2026-2027 budget allocates approximately $3.7 million for the Mosquito Control Program.

Derelict Vessel Removal: The budget provides approximately $4.9 million for derelict vessel removal, including $2.6 million in General Revenue and approximately $2.3 million from the Marine Resources Conservation Trust Fund. HB 5001E specifies that the trust fund portion is provided to FWC for grants to local governments to remove, store, destroy, and dispose of derelict vessels or vessels declared a public nuisance.

Transportation and Economic Development

Affordable Housing – SHIP: The budget provides $165.7 million from the Local Government Housing Trust Fund for the State Housing Initiatives Partnership (SHIP) Program. This is an increase of approximately $1.9 million compared to the SFY 2025-26 baseline of $163.8 million.

Affordable Housing Programs: The budget provides $70.8 million from the State Housing Trust Fund to the Florida Housing Finance Corporation for affordable housing programs. This is a major reduction from the SFY 2025-26 baseline of $221.2 million.

Hometown Heroes Housing Program: The conference report includes a supplemental FY 2025-26 appropriation of $50 million from General Revenue to the Florida Housing Finance Corporation for the Florida Hometown Heroes Housing Program, with unexpended balance reappropriated for FY 2026-27. This is $100 million below the prior-year budget of $150 million.

Job Growth Grant Fund: The budget provides $40 million in General Revenue for the Job Growth Grant Fund, with $20 million held in reserve until after January 5, 2027. This is a $10 million decrease from the SFY 2025-26 budget of $50 million and includes additional reserve/release controls.

Visit Florida: The budget provides $80 million total funds for Visit Florida, including General Revenue, State Economic Enhancement and Development Trust Fund, and Tourism Promotional Trust Fund. This is unchanged from the SFY 2025-26 budget.

Transportation Disadvantaged Grants: The budget provides $66.4 million from the Transportation Disadvantaged Trust Fund. Of this amount, $6 million is continued for the Innovative Service Development Grant program. Projects serving a single county may receive up to $750,000; projects serving multiple counties with a regional mobility goal may receive up to $1.5 million. A ten percent local match is required and all funds must be used for direct services to transportation disadvantaged clients.

Small County Outreach Program: The budget provides $81.8 million from the State Transportation Trust Fund for SCOP, including $9.0 million for municipal transportation projects under section 339.2818(7), Florida Statutes. The tax package (HB 7031E), increases SCOP’s recurring documentary stamp tax distribution from 13 percent to 16.9020 percent, generating an additional $20.0 million in recurring trust fund support for the program.

Small County Resurface Assistance Program: The budget provides $25.85 million from the State Transportation Trust Fund for SCRAP. The tax package (HB 7031E), adds SCRAP as a dedicated recipient of the documentary stamp tax transportation distribution at 3.8455 percent, generating an additional $15.2 million in recurring trust fund support for small county resurfacing needs.

Rural Infrastructure: The budget provides $27 million total for Space, Defense, and Rural Infrastructure, including $22 million from General revenue $5 million in recurring State Economic Enhancement and Development Trust Fund grant funding for Calhoun, Gadsden, Holmes, Jackson, Liberty, and Washington counties. Eligible uses include roads or other remedies to transportation impediments, stormwater systems, water or wastewater facilities, telecommunications facilities, and broadband facilities. This is an increase from the prior-year budget of $22 million.

Broadband: The conference report reappropriates the unexpended balance of funds appropriated for the Broadband Equity, Access, and Deployment Program for FY 2026-27.

General Government

Library Grants and Library Cooperatives: The budget provides approximately $22.5 million total funds for library grants and library cooperatives, including $3 million in General Revenue for library cooperatives, $17.3 million in General Revenue for library grants, and $2.15 million in Federal Grants Trust Fund. This is slightly above the SFY 2025-26 budget of approximately $21.9 million.

Fiscally Constrained County Offset: The budget provides approximately $75.2 million in General Revenue across fiscally constrained county categories, including $1.6 million for the second homestead exemption CPI adjustment, $1.4 million for conservation lands, and $72.1 million for fiscally constrained counties. This is an increase of approximately $1.4 million from the SFY 2025-26 budget of $73.8 million.

Emergency Distributions: The budget provides $35.3 million from the Local Government Half-Cent Sales Tax Clearing Trust Fund for emergency distributions. This is slightly above the SFY 2025-26 budget of $35.2 million.

Cybersecurity: The budget allocates $15 million from General Revenue to the Department of Management Services to administer a competitive grant program that provides nonrecurring technical assistance to local governments for the development and enhancement of cybersecurity risk management programs.

Back of the Bill

Sections 8 through 263 of the General Appropriations Act include several budget implementation provisions, reversions, reappropriations, and fund transfers. While many provisions are technical in nature, several items have direct or indirect impacts on counties, including:

- 911 and Telecommunications: Reappropriates prior-year funding for upgrades to 911 public safety answering points in fiscally constrained counties and funding to cover the local match share of E-Rate telecommunications projects for fiscally constrained counties.

- Cybersecurity: Reappropriates unspent funding for the State and Local Cybersecurity Grant Program, administered through the Division of Emergency Management, and continues funding for local cybersecurity assistance and matching requirements.

- Emergency Management and Disaster Recovery: Reappropriates funding for domestic security projects, the Hurricane Loss Mitigation Program, the Flood Mitigation Assistance Swift Current Program, and the required local match for Hazard Mitigation Assistance Program grants for local governments in fiscally constrained counties related to Hurricanes Debby, Helene, Idalia, and Milton. The bill also reappropriates unspent Hurricane Housing Recovery Program funds for eligible counties and municipalities impacted by Hurricanes Debby, Helene, and Milton, as well as the 2024 North Florida tornadoes.

- Federal Community Development and Energy Assistance Programs: The conference report includes several current-year back-of-the-bill appropriations through the Department of Commerce, including $73 million for CDBG-DR, $30 million for LIHEAP, $20 million for the Weatherization Assistance Program, and approximately $100 million for the Capital Projects Fund, with unexpended balances reappropriated for SFY 2026-27.

- Water Infrastructure Financing: Separately from the named water project appropriations summarized above, the Back of the Bill includes funding and reappropriation language for drinking water, wastewater, and stormwater revolving loan programs.

- Land Acquisition and Conservation: Reappropriates unexpended land acquisition funds to provide $225 million for Conservation and Rural Land Protection Easements and Agreements, with remaining funds directed toward specified conservation land acquisitions, including lands in Okaloosa County, the Caloosahatchee Big Cypress Corridor, the Ocala to Osceola Wildlife Corridor, and projects on the Florida Forever Priority List.

- Criminal Justice and Courts: Reappropriates funding for the Local Law Enforcement Immigration Grant Program, grants to assist local law enforcement agencies and county detention facilities with updated Jail Management Systems, and funding for reporting entities to modify existing systems for compliance with the Florida Incident-Based Reporting System. The bill also provides $6 million in nonrecurring funding from the Clerks of the Court Trust Fund for statutorily authorized distributions to clerks of court.

Implementing & Confirming Bills

HB 5003E—Implementing the SFY 2026-27 General Appropriations Act

The implementing bill provides the statutory authority necessary to administer the SFY 2026-27 budget and includes numerous provisions that expire July 1, 2027. The bill includes several county-relevant provisions related to Medicaid financing, public safety grants, immigration enforcement reporting, hurricane mitigation programs, and state budget administration.

County Medicaid Contributions: The bill extends the exclusion for funds specially assessed by a local governmental entity and used as the nonfederal share for the hospital directed payment program. This maintains the treatment of those locally assessed funds outside the definition of “state Medicaid expenditures” for purposes of county Medicaid contributions through July 1, 2027. The bill also continues with budget amendment authority for several Medicaid supplemental payment and financing programs, including programs supported by intergovernmental transfers or certified public expenditures.

Local Immigration Enforcement Bonuses: The bill continues authority for local law enforcement agencies to apply for immigration enforcement bonus payments. For SFY 2026-27, local agencies may apply for bonuses of up to $1,000 for eligible certified correctional officers who serve as warrant service officers or jail enforcement model immigration officers and meet the bill’s certification requirements. The local agency must certify that the county detention officer was a qualifying certified correctional officer serving in a 287(g) warrant service officer or jail enforcement model capacity for at least six months before applying.

Battery Recycling and Disposal Preemption: The bill temporarily preempts counties and municipalities from adopting or enforcing ordinances that require distributors or retailers to establish battery collection sites or collect or handle batteries and battery-containing products for off-site recycling or disposal. The preemption remains in place until a study on recommended practices for proper battery collection and handling is produced and expires July 1, 2027. Specific Appropriation 1820 in HB 5001E provides $100,000 in nonrecurring General Revenue to the Department of Environmental Protection to competitively procure the study, which must include recommendations on safety standards, employee training, and liability issues related to fire, environmental harm, and public health and safety risks. The final report is due June 30, 2027.

Immigration Detainer Records and Fingerprinting: The bill creates a new requirement for law enforcement agencies to electronically submit fingerprints for qualifying offenders in custody who are subject to immigration detainers. FDLE must create records containing immigration detainer information, and the bill establishes an administrative expunction process for records made contrary to law or by mistake.

Drone as First Responder Grant Program: The implementing bill creates the Drone as First Responder Grant Program within FDLE to provide funding to law enforcement agencies, fire service providers, ambulance crews, and other first responders for the purchase of compliant drones. Local governments may apply on behalf of one or more agencies. Grants are awarded on a first-come, first-served basis and require at least a 50 percent local match, which FDLE may waive for agencies solely serving fiscally constrained counties. Awards are capped at $250,000 per agency and $50,000 per drone.

My Safe Florida Home Program: The implementing bill revises the My Safe Florida Home Program, including eligibility and application provisions, and modifies eligible mitigation improvements by reorganizing opening protection and roof improvements and adding roof covering replacement as an eligible roof-related improvement. County building departments may see additional permitting and inspection activity because all mitigation work funded through the program must secure required local permits and inspections and be performed by properly licensed contractors.

Payment Scam Study: The bill directs FDLE to conduct a study on payment scams, including spoofed calls, scam text messages, malicious advertisements, business e-mail compromise, consumer education, and law enforcement strategies. FDLE must submit a report by February 1, 2027, including any legislative or regulatory recommendations and recommendations to improve coordination among federal, state, local, and tribal authorities.

HB 7031E—Tax Package

HB 7031E is the agreed-upon tax package in the Special Session E budget conference report. The bill makes broad changes across property tax administration, ad valorem assessment limits, sales tax exemptions and holidays, documentary stamp tax distributions, transportation funding, gaming taxes, and tax credit programs. Below are additional county-related impacts:

Ad Valorem Assessment and Tax Base Changes

Mobile Home Park Assessment Cap: The bill creates a new assessment limitation for qualifying mobile home parks beginning with the 2027 ad valorem tax roll. If at least 75 percent of the lots in a mobile home park are subject to written rental agreements of at least one year and the park’s ad valorem taxes are required to be passed through proportionately to mobile home owners, the property must be assessed using the prior year’s assessed value as the base, with annual assessment increases capped at 3 percent, similar to homesteaded properties. Mobile home park owners must apply annually to the property appraiser by March 1 and provide documentation required by the Department of Revenue.

Portability of Prior Homestead: The bill conforms homestead portability language to the State Constitution beginning with the 2027 ad valorem tax roll by removing references to an “immediate” prior homestead. The change clarifies that the portability calculation applies to the prior homestead abandoned within the allowable three-year period, while retaining the existing $500,000 portability cap.

Agricultural Classification for Compost: Beginning with the 2027 property tax roll, the bill expands the definition of “agricultural purposes” to include compost derived entirely from agricultural activity and regulated under s. 403.7043, F.S. This may allow land used for qualifying agricultural composting activity to receive or retain agricultural classification, which can reduce the property’s assessed value compared to non-agricultural assessment.

Agricultural Property Assessments — Packinghouses: Beginning with the 2027 tax roll, the bill creates a new assessment provision for certain packinghouses used for fruits and vegetables. A qualifying packinghouse and the land on which it is located may be treated as part of the agricultural income methodology and have no separately assessable contributory value if used exclusively for processing fruit or vegetable products harvested from commonly owned agricultural land. This may reduce taxable value for qualifying agricultural packinghouse property, depending on how the property is currently assessed.

Children’s Services District CRA Exemption: The bill adds special districts created under s. 125.901, F.S., to the list of public bodies or taxing authorities exempt from community redevelopment trust fund contribution requirements. This may affect CRA tax increment calculations in jurisdictions where a children’s services district overlaps with a community redevelopment area.

Property Tax Administration and Transparency

Real Estate Listing Platforms: Beginning February 1, 2027, online residential real estate listing platforms must include estimated ad valorem taxes for listed Florida residential property. Platforms may not use the current owner’s taxes as the basis for the estimate when using a tax estimator or buyer payment calculator. The Department of Revenue must annually publish a tax estimate formula and countywide aggregate average millage rate beginning December 15, 2026, and county property appraisers must provide DOR with information needed to develop those estimates, including tax district codes and millage information. FAC supported this change as part of HB 827/SB 856.

Property Tax Administration: The bill also makes several administrative changes affecting property appraisers, tax collectors, and value adjustment boards. Property appraisers and tax collectors must post their final approved budgets and supporting schedules on their official websites within 30 days after adoption, and county websites must link to those postings or host the documents if the constitutional officer does not have an official website. The bill also revises exemption denial notice procedures by requiring property appraisers to serve disapproval notices before TRIM notices are mailed when additional information is obtained after July 1. In addition, the bill updates the deployed servicemember exemption and related refund procedures, expands certain homestead protections for military members and specified federal employees stationed outside Florida, and revises value adjustment board hearing authority for certain property tax appeals.

Millage Governance and School Tax Procedures

Voting Threshold for New MSTU and Dependent District Millage: The bill requires the initial millage rate for a newly levied dependent special district or MSTU to be approved by unanimous vote of the governing body, by a three-fourths vote if the governing body has nine or more members, or by referendum. After the first year, future millage increases are governed by the standard rolled-back rate and maximum millage procedures. FAC opposed the unanimous vote threshold because it may limit counties’ ability to use targeted service-area funding for local needs.

Commissions Paid on Voted School Levies: The bill expands the county commission payment obligation for tax collector commissions related to school millages. Current law requires the board of county commissioners to pay tax collector commissions on non-voted school millages and certain additional school taxes related to homestead exemption differences. HB 7031E extends that framework to voted school millages, while allowing the tax collector to waive the commission for those voted levies. A waiver must be communicated to the board of county commissioners by September 1, 2026, for the 2026 calendar year and, thereafter, by March 1 for the fiscal year beginning October 1. FAC supported efforts to address the issue but remains concerned about shifting school district tax collection costs to county commissions.

Voted School Millage Ballot Placement and Timing at General Election: The bill revises procedures for district school millage elections to clarify the roles of the school board and county commission. Under current law, the county commission is responsible for calling the election for a school district millage referendum, even though the millage is proposed by the school board. HB 7031E provides that the school board must adopt the resolution calling for the election and provide the ballot title and wording. The county governing body must then place the measure on the ballot for the next general election held more than 90 days after the school board adopts the resolution. The change clarifies that the school board is responsible for proposing the voted school millage, while the county’s role is limited to ballot placement.

Sales Tax Exemptions and Holidays

The bill includes several sales tax exemptions and holidays including:

- Expands the annual back-to-school sales tax holiday to run from July 20 through August 20 for qualifying clothing, school supplies, learning aids, and personal computers or accessories;

- Creates a refund-based sales tax exemption of up to $500 for qualifying home-hardening products purchased for eligible homestead property from July 1, 2026, through June 30, 2029;

- Exempts portable gas or diesel fuel cans of 5 gallons or less and propane tanks of 20 pounds or less;

- Creates a hunting, fishing, camping, firearms, and ammunition sales tax holiday from September 1 through December 31, 2026;

- Creates a refund process for sales tax paid on certain public works materials purchased by contractors for state universities and Florida College System institutions; and

- Provides admissions tax exemptions for certain major tennis tournaments through July 1, 2029.

Documentary Stamp Tax Distributions and Transportation Funding

The bill revises the distribution of documentary stamp tax revenues by increasing the amount directed to the State Transportation Trust Fund and creating new dedicated transfers for transportation and water infrastructure purposes. Under current law, the lesser of 20.5453 percent of the documentary stamp tax remainder or $360.08 million is distributed annually to the State Transportation Trust Fund. HB 7031E increases that annual cap to $395.28 million and revises how those transportation dollars are allocated among state transportation programs. The bill also creates two new $60 million annual transfers: one to the Water Protection and Sustainability Program Trust Fund for the C-51 Reservoir Project and one to the State Transportation Trust Fund for the Florida Rail Enterprise.

The revised distribution increases the overall documentary stamp tax transfer to the State Transportation Trust Fund and directs the incremental transportation funding toward small county road programs. SCOP’s share increases and SCRAP is added as a new dedicated recipient, while the percentage shares for SIS and TRIP are reduced. Based on the capped distribution amounts in the bill, SIS and TRIP appear to remain approximately level in nominal dollars, but receive a smaller percentage share of the transportation distribution.

- State Transportation Trust Fund: The annual documentary stamp tax distribution cap increases from $360.08 million to $395.28 million, an increase of $35.2 million.

- Small County Outreach Program (SCOP): SCOP’s share of the transportation distribution increases from 13 percent to 16.9020 percent. Based on the new distribution cap, this represents approximately $20 million in additional funding for SCOP.

- Small County Road Assistance Program (SCRAP): SCRAP is added as a dedicated recipient of the transportation distribution at 3.8455 percent, representing approximately $15.2 million in funding.

- Strategic Intermodal System (SIS): SIS’s percentage share is reduced from 78 percent to 71.0540 percent. However, because the overall transportation distribution cap increases, SIS remains approximately flat in dollar terms.

- Transportation Regional Incentive Program (TRIP): TRIP’s percentage share is reduced from 9 percent to 8.1985 percent. Similar to SIS, the lower percentage is applied to a larger distribution amount, leaving TRIP approximately flat in dollar terms.

- C-51 Reservoir Project: The bill creates a new $60 million annual transfer to the Water Protection and Sustainability Program Trust Fund for the C-51 Reservoir Project.

- Florida Rail Enterprise: The bill creates a new $60 million annual transfer to the State Transportation Trust Fund for the Florida Rail Enterprise.

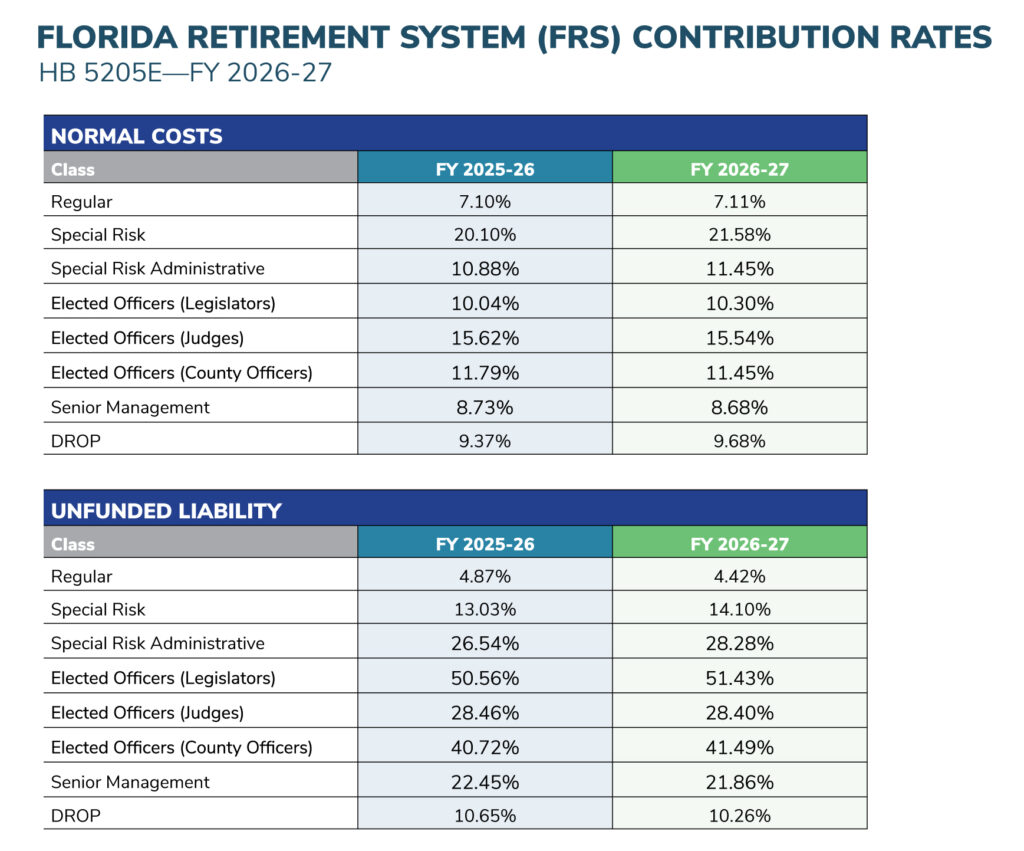

HB 5205E—Florida Retirement System

HB 5205E revises Florida Retirement System (FRS) employer contribution rates for SFY 2026-2027, effective July 1, 2026. The bill updates both the normal cost rates and the unfunded actuarial liability rates for each FRS membership class, including Regular Class, Special Risk Class, Elected Officers, Senior Management, and DROP. The overall rate package is estimated to have a net statewide county impact of approximately $102.5 million.

The primary policy driver in the bill is the creation of a minimum cost-of-living adjustment for eligible Special Risk Class retirees. Beginning July 1, 2026, eligible Special Risk retirees and annuitants will receive an adjusted monthly benefit equal to the greater of the current statutory calculation or 1.5 percent of the benefit, after the fifth anniversary of retirement. This Special Risk COLA provision is estimated to have a statewide employer impact of approximately $173 million on counties. This was a policy choice agreed to during the waning hours of the special session budget over the holiday weekend.

The bill also makes targeted policy changes related to the Deferred Retirement Option Program (DROP), allowing an elected officer, except while serving as a legislator, to remain in elective office and receive accumulated DROP proceeds after reaching age 59½. The bill further requires the Division of Retirement or State Board of Administration to recoup certain DROP proceeds if the elected officer later becomes subject to benefit forfeiture provisions.

The charts below show the revised employer contribution rates for: 1) normal plan costs and 2) the unfunded actuarial liability of the system.

Leave A Comment

You must be logged in to post a comment.